Investing for a Longer Life: Why 120 is the New 100

Like many things in life, with investing it’s important to focus most your time and efforts to getting the big things right instead of squandering your time on the less meaningful things. Determining the proper asset allocation in a portfolio is the single most important factor for achieving long-term investment goals 1, much more than trying to find the next great stock. Unfortunately, with the media and financial ads producing more and more hyperbolic headlines about hot stocks, funds and strategies, it has become much easier to lose track of asset allocation’s critical role with your retirement portfolio.

Asset allocation is the process of divvying up your portfolio into different asset classes like stocks and bonds. Effective asset allocation is critical to arrive at the needed overall returns in your lifetime. As an investor, it may be time to re-evaluate traditional allocation rules of thumb and consider new approaches for building enough wealth in retirement.

Here is why you should be planning your investments with a longer time-horizon and why 120 may just be the new 100.

The 100 Rule of Thumb

For many years, a widely used rule of thumb used by financial professionals and investors to simplify asset allocation was the rule of 100. It states that an investor should hold a percentage of stocks equal to 100 minus his or her age. For example, a 60-year old would have 40% of their holding in stocks. The rest would be held in relatively safer investments like bonds and cash.

This rule has been a helpful starting point for investor asset allocations in the past. However, two factors are calling this rule of thumb into question.

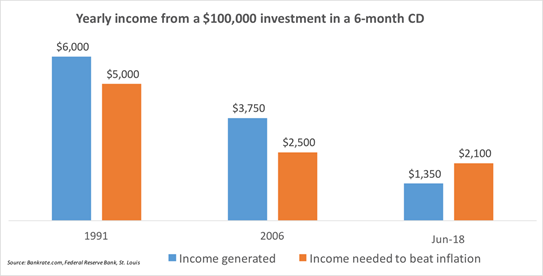

The first factor is the level of interest rates. Inflation and low interest rates can make the case for holding a higher allocation of stocks. An investor’s holdings in stocks have traditionally decreased the closer he or she gets to retirement with the goal of removing “too much” risk. However, bond yields have remained stubbornly low especially after accounting for inflation. This continues to be a major challenge for investors, especially those that are preparing for retirement or already in their golden years. The current low yield era has made is very challenging for retirees to fund their desired lifestyle. The 100 Rule of Thumb may be too conservative for what investors need.

The second factor is that we are living longer. Many people continue to undershoot how long they will live. A recent survey by the Society of Actuaries showed that over 40% of retirees underestimate their life expectancy by over five years. So, that means that many Americans will likely live longer than they think, thanks to better healthcare and improved lifestyle choices. The chart below illustrates how our longevity is changing: The bottom line is that you want your investment allocation to support your life for your entire life.

Why Using 120 Instead of 100 Makes More Sense

Using a single rule of thumb based on age is not a complete tool for asset allocation since it does not consider risk tolerance, nest eggs and job security. However, excessively high allocations to bonds and cash can be the single biggest impediment to achieving retirement investment goals.

Yes, the experience of the great recession in 2008 followed by numerous stock market downdrafts over the last decade has made many investors more risk averse. However, investors can really suffer by staying out of the market or carrying excessively high allocations to conservative, inflation-losing investments.

In fact, a Wells Fargo retirement study found that 60% of polled investors focus more on avoiding loss than compounding growth of their investments for retirement. This conservative stance actually did not vary much across age ranges: 59% of 30-somethings, 62% of 40-somethings, 58% of 50-somethings, and 52% of those 60+ agree with that approach. 2

Need To Fix Your Mix? Just Do It

Regardless of whether it’s a 100 or 120 Rule of Thumb, it’s important to actually implement your appropriate asset allocation once you have balanced your age with your risk tolerance, future goals and needs. It’s never too late to get started. Asset allocation is not a one-time event as it’s a lifelong process of remeasurement and fine-tuning. At a time when adults are living longer and getting less income benefits from “safer” investments, it might be time to consider adjusting to the 120 Rule of Thumb. If you have questions about whether or not your investments are poised to help you reach success, feel free to reach out to me at dhone@lcvadvisors.com.

1 Roger Ibbotson “The importance of asset allocation” Financial Analysts Journal 2010.

2 2016 Well Fargo Retirement Study