Let's Get Real

Inflation can be the biggest challenge investors face over time aside from behavioral hurdles including regret, fear of missing out etc. The good news is that inflation remains subdued with the rate currently below 2%1. This level is much lower than runaway inflation of the 1970s and early 1980s when the Prime borrowing rate notched 21.5% (Dec 1980) compared to a Prime rate of 3.25% today. In the early 80’s with the Prime rate peaking, a 30-year fixed-rate mortgage also topped 18.5% (including 2 points!)2. That should make everyone feel better about their current mortgage.

A tricky thing with inflation is it can be hard to measure since there are many moving parts that are included in the figure. Though inflation has averaged roughly 2-3% over the last two decades, the chart below shows the volatility of the components, both inflationary or deflationary.

Over the last few decades, we have benefited by the incredible improvements in quality, performance and price across many goods and services. Below is an ad from Radio Shack from 1991 which shows all of the electronics that one would have to buy to replicate today’s Apple iPhone (stereo, clock, computer, camcorder, mobile phone, answering machine etc.). It’s amazing to consider these technological advances that have improved our quality of life while helping to offset inflation over decades.

Losing Money Safely

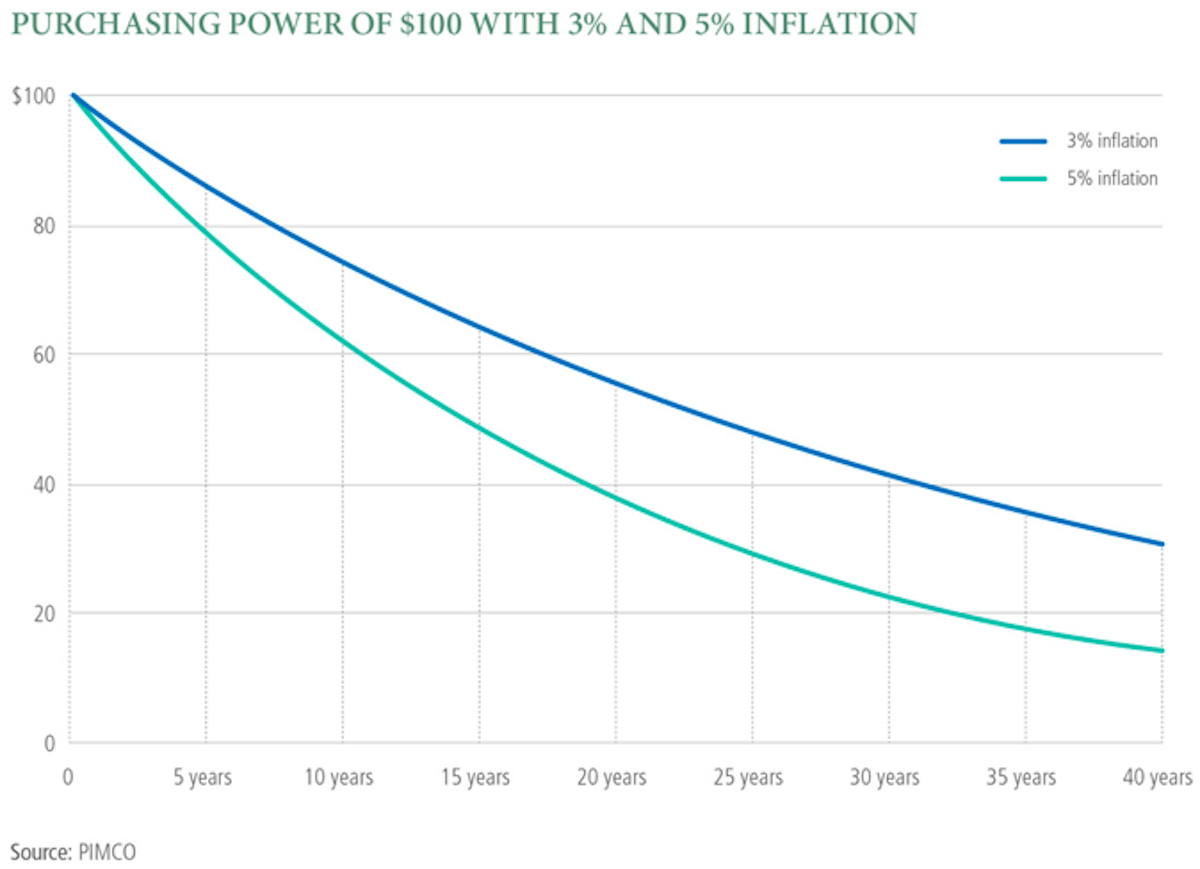

Even with inflation close to generational lows, investors should be mindful of the corrosive effects on purchasing power over time. With checking accounts paying a measly 0.01%3 and using an inflation rate of 2%, one is losing money in real interest terms. Real interest is defined by subtracting inflation from interest rates on deposits. In the earlier example of 0.01% interest, after accounting for 2% inflation, one is losing 1.99% a year in real terms. The chart below shows the corrosive impact of inflation (at 3% and 5% rates) on your savings over the longer haul.

While savers can receive interest in a safe and federally insured checking account or CD, in real terms, the saver is actually losing money, albeit safely. This is the “stealth” threat or thievery to investors longer-term as it erodes real savings and purchasing power which are critical ingredients for retirement investing success

Inflation Trouncing Income Over The Last Decade

The Stock Market: Rising & Falling Inflation Is The Focus

With interest rates near historic lows, a big question is how will the stock market perform in a sustained inflationary environment? Over the longer term, the market appears to be more sensitive to inflation rising or falling than the actual levels (see the table below). The stock market has clearly performed much better during a falling inflation rate versus rising inflation. However, the average 6.7% return during periods of rising inflation is still respectable, especially in real terms.

Source: New York University, Ben Carlson

Inflationary Theft: Get Real

A key retirement investing goal is to increase long-term purchasing power by generating a real investment return over time. Many investment strategies are available today to help combat the eroding impact of inflation. Options include corporate bond funds, floating-rate bond funds, inflation-protected securities funds and dividend growth-oriented stocks and funds. Understanding inflation and its real impact is an important step for an inflation fighting plan with retirement investing.

1. Federal Reserve Bank of St Louis

2. Freddie Mac

3. J.P. Morgan Chase rates as of 2/16/21.